Introduction: A “Building Problem” That Exposes a “System Problem”

In June 2026, residents and owners of Flair Towers in Mandaluyong, Metro Manila reported a scenario that should make any overseas buyer pause: a serious dispute between the condo corporation (homeowners/condo association structure) and the developer-linked property management company escalated to the point where the management team allegedly withdrew abruptly, leaving day-to-day operations in a state of confusion.

People described practical consequences that sound small until they happen to your asset:

- official communication channels disrupted

- maintenance and repair workflows slowed or inaccessible

- operational coordination and security routines thrown into uncertainty

If you live in the building, you can show up, ask questions, attend meetings, and push for action.

If you are an overseas owner, you often learn about it late—and you have fewer ways to respond quickly.

I’ve spent years living and working across countries with a “risk controller” mindset. My conclusion is simple:

Flair Towers is not just a one-off “property drama.” It’s a case study in how Philippines condo ownership can become a cross-border governance problem—especially for absentee investors.

If you’re considering buying (or already own) a condo in Manila, this article breaks down three system-level risks that marketing brochures rarely explain.

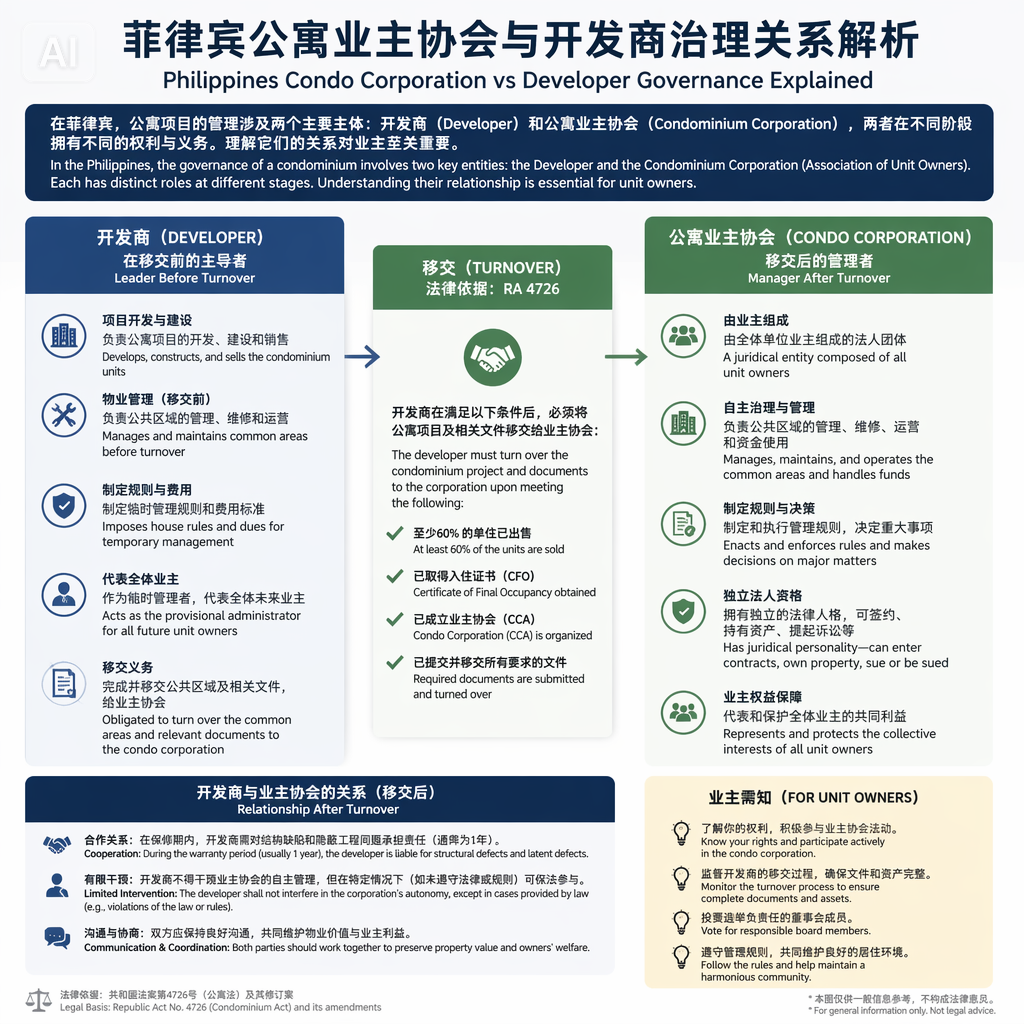

Risk #1 — The Hidden Power Shift: Developer vs. Condo Corporation Governance

Many foreign buyers focus on the developer brand: DMCI, Megaworld, SMDC, and others. The assumption is understandable: “Big developer = safer investment.”

But Philippines condo ownership has a governance structure that surprises overseas investors.

In many condo setups, once a building reaches a certain stage of turnover/occupancy, a condo corporation / homeowners association (the collective ownership body) becomes the key governing entity for building operations. That creates a structural tension:

- The developer (or its affiliated company) often wants a management structure that supports predictable fees and vendor control.

- Unit owners (through the condo corporation) increasingly demand transparency, accountability, and tighter cost oversight.

When both sides cooperate, things look smooth.

When they don’t—especially during disputes involving budgets, billing, contracts, or governance—building operations can become the battlefield. And when that conflict escalates, the people caught in the middle are usually:

- tenants (who just want repairs and stable services)

- on-site residents (who experience daily disruption)

- overseas owners (who lose visibility and reaction speed)

The hard truth: you may think you bought a passive “rental asset,” but you also bought into a local governance system that can change direction quickly.

Risk #2 — “App-Based Management” Can Collapse Into a Physical Blind Spot

A popular sales narrative for overseas buyers goes like this:

“Don’t worry. Everything is managed. You can collect rent and handle issues from your phone.”

That can be true—when the system runs normally.

But cross-border property management has a fragile dependency: your visibility is only as good as the local workflows. If digital channels (apps, portals, official email systems, ticketing tools) become unreliable during management transitions or disputes, overseas ownership can feel like managing a property through fog.

What does that look like in real life?

- Repairs slow down → tenants lose patience

Manila’s climate (heat, humidity, typhoons) turns “minor maintenance” into fast deterioration. If leaks, mold, AC issues, or plumbing problems aren’t handled quickly, tenants don’t wait politely. They negotiate hard, withhold rent, or move out. - Deferred maintenance compounds

In tropical conditions, an empty unit doesn’t “pause.” Paint, ceilings, walls, and fixtures degrade faster without consistent upkeep. - Cross-border coordination cost spikes

The moment you can’t rely on stable building processes, your “remote ownership” turns into coordination work—calls, vendor sourcing, follow-ups, and sometimes costly in-person trips.

This is why I treat “one-tap property management” as a best-case scenario, not a guaranteed baseline.

Risk #3 — The Secondary Market Can Lock Up Faster Than People Expect

When a building faces a reputation shock—whether it’s operational disruption, governance conflict, or public controversy—many investors think:

“Fine. I’ll sell. Even at a discount.”

This is where Manila can surprise you.

Compared to more centralized, highly standardized resale markets, Manila’s condo resale ecosystem can feel fragmented:

- pricing discovery varies widely

- buyer pools can be narrow for certain segments

- transaction processes can be slower and more document-intensive than many first-time foreign buyers assume

And even if you find a buyer, the math can still hurt.

The “paper profit” problem

Developers can continue marketing new units at higher headline prices, while resale demand stays thin. This can create a psychological trap: your unit looks valuable on paper, but liquidity is limited when you urgently need an exit.

Transaction friction and holding costs

Selling can involve meaningful costs (taxes, fees, transfer-related expenses, agent commissions), while ongoing holding costs continue in the background (condo dues/association fees, repairs, vacancy months).

Demand mismatch risk

In prime areas (Makati, BGC, Mandaluyong), pricing can drift toward “international city” levels. But local income levels may not support premium rents at scale. That can leave the market relying heavily on:

- expats with shifting demand cycles

- specific industries (which can boom and fade)

- foreign buyers’ sentiment (which can change quickly)

When the marginal buyer disappears, liquidity can disappear with them.

A Risk Controller’s Checklist: How to Approach Philippines Condos Without Losing Control

I don’t believe in “never buy in the Philippines.” I believe in buying only when the decision can survive worst-case scenarios.

If you want practical guardrails, here are three:

1) Treat the foreign ownership limit as a hard boundary (not a workaround game)

Philippines condo foreign ownership is commonly discussed around the 40% foreign ownership cap at the project/building level. Before committing funds, verify eligibility and compliance through proper documentation and professional review.

If your “solution” depends on informal workarounds, your risk profile is no longer “real estate.” It becomes “legal and enforceability uncertainty.”

2) Don’t buy purely for yield unless you can personally use the asset

If the only reason you’re buying is a promised rental return, you’re exposed to too many variables you don’t control: vacancy, tenant quality, maintenance, governance conflicts, and resale liquidity.

A stronger approach is practical utility:

- Can you use the unit as a personal base?

- Can it support your cross-border work/life needs?

- Would you still be comfortable holding it if rent drops or vacancy lasts 6–12 months?

If the answer is no, the “investment” is fragile.

3) Stress-test your cash flow model (assume higher holding cost + longer vacancy)

A conservative model is not pessimism; it’s how you stay solvent.

Before you buy, run scenarios like:

- higher maintenance frequency than expected

- longer vacancy periods

- slower repairs and higher coordination costs

- additional selling friction and longer time-to-exit

If your finances still hold under stress, you’re buying from strength—not hope.

The Bottom Line

Flair Towers—whether you view it as a management dispute, a governance conflict, or a cautionary headline—highlights a deeper issue:

Overseas property ownership is not only about purchase price and rent. It’s about governance, visibility, and liquidity under pressure.

If you’re buying in Manila, the question is not “Is this building modern?” or “Is the developer famous?”

The question is:

Can I defend this decision if the worst-case operational scenario happens—and I’m not physically there?

That is what “cross-border risk control” really means.